Cybersecurity is the place where technology, geopolitics, and business strategy meet – and it’s evolving faster than almost any other sector. Every year, cyberattacks grow more sophisticated, businesses become more dependent on digital infrastructure, and governments step up regulations, making security an absolute necessity, not a luxury. And, look, cybersecurity isn’t just growing: year after year, it’s become a bigger slice of global IT spending, with companies prioritizing security, even in downturns. So when it comes to long-term investment themes that offer growth and resilience, cybersecurity seems like, well, a lock.

Thesis

Cyber threats are relentless:

Cybersecurity is a must-have for businesses and governments. In this industry, revenues are resilient – even in downturns – with global investment projected to more than double between 2024 and 2030.

Growth factors:

The industry’s growth has been fueled by a mix of factors: increasing cyberattacks, the shift to cloud and remote work, and stricter regulations that force businesses to beef up security.

Cloud-based security and software subscriptions:

These deliver high-margin, recurring revenue. Companies providing these services benefit from strong pricing power, high customer retention, and scalable business models – making them the fastest-growing cybersecurity segment.

Investment profiles:

Pure-play cybersecurity firms offer high growth but can be volatile, while diversified tech companies provide stability, strong cash flows, and lower risk.

Balance in the industry:

Incumbents and disruptors together balance stability and growth. Cybersecurity ETFs offer broad exposure to the industry but may include weaker players, making individual stock selection a more focused approach.

Risks

Many cybersecurity stocks trade at lofty valuations. So market corrections, rising interest rates, or slowing growth could lead to serious price swings, especially for high-growth, unprofitable companies.

This industry is highly competitive and is known for rapid-fire innovations. Companies that fail to keep up risk losing market share to more agile players.

A few Big Tech firms bundle security solutions into their existing products, which makes it harder for standalone cybersecurity companies to compete on price, scale, or enterprise.

Business customers constantly reassess their security needs. Shifts in preferred security models, new compliance requirements, or changing customer preferences can quickly alter a cybersecurity company’s growth trajectory.

A big-picture look at the industry and its growth:

Cybersecurity is one thing that companies and governments just can’t skimp on – no matter what the economy’s doing. Rising cyber threats, cloud adoption, and continually evolving regulations are all making this industry a high-growth, all-weather place to invest.

Cybersecurity isn’t just another slice of the tech pie – it’s one of the few industries where demand seems to travel in only one direction: up. Every year, cyberattacks have become more sophisticated, businesses have become more reliant on digital infrastructure, and regulations around data security have tightened. That chilling cocktail has made cybersecurity an essential, non-negotiable expense. Unlike consumer tech or software – which can struggle in downturns – cybersecurity is something businesses can’t afford to trim. After all, the alternative is being hacked, losing millions, and seeing reputations damaged forever.

That’s why, even when the economy was shaky in 2022-23, average cybersecurity outlays still grew by around 6%, and took up a greater share of overall IT spending. It’s a rare "all-weather" industry – one that’s resilient during downturns but still benefits from long-term growth. And that growth is huge: in 2024, global cybersecurity spending was about $245 billion, and forecasts see it expanding at a compound annual growth rate (CAGR) of 12.9%, more than doubling in size by 2030. That’s a level of expansion that few industries can match.

So what’s fueling all that growth? Three key factors:

Expanding threat landscape: Cyberattacks are bigger, bolder, and more expensive than ever. In 2023, the average cost of a data breach hit nearly $4.5 million globally – a 10% increase from the year before. Ransomware, nation-state hacking, and cyber warfare (as seen in recent conflicts) have all turned cybersecurity into a national defense priority. Governments, hospitals, and entire infrastructure networks are at risk, so spending on security is not optional.

The move to cloud and remote working: As businesses embrace the cloud, traditional security models have become almost obsolete. With employees working remotely from multiple devices and accessing company data from anywhere, there’s explosive demand for cloud-based security, stricter access controls (like Zero Trust models), and AI-driven threat detection.

Security regulations: Governments worldwide are cracking down on organizations with lax security. New regulations mean companies can face fines for data breaches, and as cyber threats increase, compliance requirements are only going to get stricter, making cybersecurity a permanent and growing expense for every major company.

Honing in on its components

Cybersecurity isn’t just one thing – it’s a multi-layered system with different players specializing in various aspects of digital security. Some companies build software tools that stop attacks, others make the hardware infrastructure that businesses rely on, and some provide managed services to help organizations stay ahead of threats.

Software and cloud-based providers: At the core of the industry, these companies develop solutions like firewalls, endpoint protection, and cloud security platforms. They sell products through software licenses, enterprise contracts, and subscription plans. Think of it as similar to streaming services charging for access, except here they’re protecting businesses from hackers.

Hardware and infrastructure companies: These firms build the physical devices – firewalls, routers, and intrusion-detection systems – that defend networks against cyber attackers. Although cloud-based security is the future, many industries still require on-premise protection, and these companies create hybrid systems that combine physical and digital shields.

Managed Security Service Providers (MSSPs): These providers offer outsourced cybersecurity services for companies lacking in-house expertise. They deliver continuous monitoring, threat detection, and real-time response, which is essential for round-the-clock protection as cyberattacks become more complex.

Competitive advantages

Castles have deep and deadly waters around them to keep disruptors at bay, and companies have “competitive moats” that serve as barriers to entry. Here’s a look at the industry’s competitive dynamics:

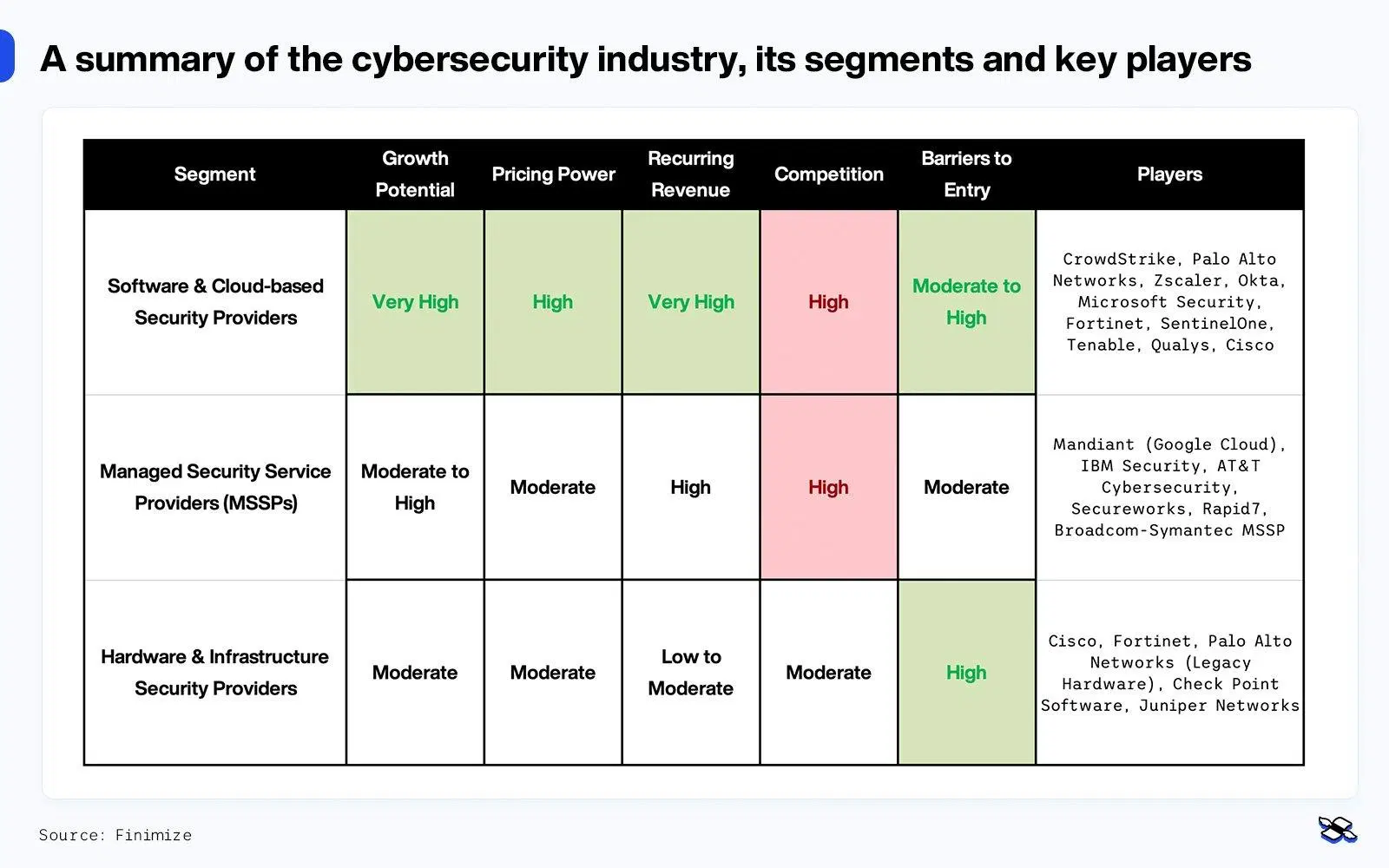

Software and Cloud-based Security Providers

Growth potential:

Very High. The fastest-growing segment, fueled by cloud adoption and digital transformation, often shows double-digit revenue jumps.

Pricing power:

High. With mission-critical solutions like Zero Trust and Endpoint Security, these firms charge premium prices because their software is deeply integrated into enterprise IT infrastructures.

Recurring revenue model:

Very High. Dominated by SaaS subscription models, these companies enjoy high-margin, recurring revenue from multiyear contracts that create sticky customer relationships.

Level of competition:

High. Dominant players and niche firms compete fiercely, leading to frequent mergers and acquisitions.

Barriers to entry:

Moderate to high. Although building a cloud security product can be relatively quick, scaling it to an enterprise-grade solution requires proven track records and sizable customer bases.

A few things to think about: Despite an attractive profile, this segment is fiercely competitive. Pure-play cybersecurity firms need to offer superior technology or focus on niche needs. The rapid pace of innovation means that failing to keep up with emerging threats can render a company obsolete.

Players: CrowdStrike, Palo Alto Networks, Zscaler, Okta, Microsoft, Fortinet, SentinelOne, Tenable, Qualys, Cisco.

Hardware and Infrastructure Companies

Growth potential:

Moderate. Demand for physical security gear remains steady, although the shift toward cloud-based security puts pressure on traditional hardware solutions.

Pricing power:

Moderate. While some companies have carved out niches with differentiated products, overall, hardware faces a price squeeze as markets lean toward software-based security.

Recurring revenue model:

Low to Moderate. Revenues largely come from one-time hardware sales, though some firms are shifting to hybrid models.

Level of competition:

Moderate. Legacy players dominate, but cloud adoption is gradually shifting market dynamics.

Barriers to entry:

High. Developing and manufacturing security hardware requires deep expertise, significant R&D, and robust supply chain capabilities.

A few things to think about: Hardware security firms may offer stability, cash flow, and entrenched market positions. Investors looking for income-focused opportunities might favor these firms for their dividends and reliable cash flows.

Players: Cisco, Fortinet, legacy hardware divisions of firms like Palo Alto Networks, Check Point Software, Juniper Networks.

Managed Security Service Providers (MSSPs)

Growth potential:

Moderate to High. With increasing cyber threats, more enterprises are outsourcing security operations.

Pricing power:

Moderate. The competitive nature of this segment keeps pricing in check, as customers can often switch providers more easily than with SaaS-based software.

Recurring revenue model:

High. Long-term contracts ensure revenue stability, though margins tend to be lower due to labor-intensive service models.

Level of competition:

High. Both regional and global MSSPs, along with major cloud providers, compete for market share.

Barriers to entry:

Moderate. While starting an MSSP requires significant talent and resources, low differentiation among providers makes it easier for new players to enter.

A few things to think about: MSSPs may be attractive acquisition targets for larger cybersecurity vendors seeking to offer a complete suite of services. However, their lower profit margins and scalability challenges often make them more of a supporting component alongside higher-growth software firms.

Players: Google Cloud’s Mandiant, IBM Security, AT&T Cybersecurity, Secureworks, Rapid7, Broadcom’s Symantec.

If you’re investing in cybersecurity for the long haul, software and cloud security may be your best bets. These companies benefit from high margins, recurring revenue, strong pricing power, and the ability to scale rapidly without the overhead costs of hardware or services. As businesses shift to cloud-based security and AI-driven threat detection, software firms are neatly positioned for substantial long-term growth. That’s why many of the best-performing cybersecurity stocks are pure-play software companies with SaaS-based models – compounding revenue over time and maintaining sticky customer relationships through multi-year contracts.

Not every investor has the same risk appetite, however. If you’d rather prioritize stability over high growth, managed security service providers (MSSPs) offer a steadier, albeit lower-margin, business model. Similarly, hardware and infrastructure security firms provide a more value-oriented approach with predictable cash flows and dividends, ideal for income-focused investors.

How to invest in cybersecurity

It’s a big and growing industry – cybersecurity’s high-growth stocks are volatile, but they offer the potential for strong returns. Diversified tech firms deliver stability and cash flow while still benefiting from overall industry expansion. As an investor, you can choose based on your risk tolerance or consider a balanced portfolio approach.

When building a cybersecurity investment portfolio, two key principles come into play: scale and innovation.

Diversified tech giants:

Larger firms like Microsoft and Cisco form a solid foundation due to their entrenched market positions and ability to bundle security solutions with broader enterprise offerings. Their scale, long-forged relationships, and cross-selling abilities provide a stable base.

High-growth disruptors:

Leading pure-play cybersecurity firms such as Fortinet, Palo Alto Networks, CrowdStrike, Zscaler, and SentinelOne are laser-focused on specific security solutions. They drive long-term growth with innovations in Zero Trust security, AI-driven threat detection, and cloud-based protection, though they may trade at higher valuations and with more volatility.

This balanced approach captures both the defensive stability of big tech and the high-growth potential of next-gen security solutions.

If you’re looking for an easier way to invest in cybersecurity, there are ETFs that offer diversified exposure to the industry. While these ETFs hold a basket of cybersecurity stocks and spread risk, they may include overvalued or weaker names, which is why some investors prefer to handpick their investments.

Final thought

If you're more risk-averse, you can allocate more of your intended investment toward diversified tech giants like Microsoft and Cisco, which offer cybersecurity as part of a broader business. These stocks tend to be less volatile due to robust cash flows, providing a safer way to invest in cybersecurity while still benefiting from industry growth. Conversely, if you're comfortable with higher risk and seek direct exposure to rapid expansion, pure-play stocks offer the potential for sweeter long-term returns, albeit with more volatility.

Portfolio Strategy Overview

Foundation:

Heavier, diversified technology firms provide stability.

Innovation:

Leading pure-play cybersecurity firms bring high-growth potential.

Balanced exposure:

Combining both types of companies ensures a portfolio that captures both defensive stability and innovative disruption in the cybersecurity space.

Key financial metrics summary of portfolio companies

When choosing where to invest, consider metrics such as revenue growth, profitability, recurring revenue ratios, and market valuation. A well-rounded approach allows you to balance high-growth opportunities with stable, dividend-paying tech giants.

Cybersecurity remains one of the most compelling long-term investment themes available. Whether you prefer the innovation and rapid expansion of pure-play software companies or the stability and cash flow of diversified tech giants, there’s an opportunity to build a portfolio that aligns with your risk tolerance and investment goals.

---

Capital at risk. Our analyst insights are for educational and entertainment purposes only. They’re produced by Finimize and represent their own opinions and views only. Wealthyhood does not render investment, financial, legal, tax, or accounting advice and has no control over the analyst insights content.

Join the Investors' Club

Get access to professional investing tools for free and start building your wealth today!

Capital at risk