The sharp decline in the value of the Japanese yen in 2023 means that European stocks have higher returns than Japanese ones this year.

Lower inflation in 2024 would likely lead to a further boost for European stocks that look cheap relative to history despite their recent rally.

Corporate governance reforms have been a game-changer in Japan, fueling new hopes that the Japanese economy may finally be leaving its low-inflation and low-growth ways in the past.

Tempting as it may seem after a year like 2023 to devote your entire stock portfolio to the S&P 500, it wouldn’t be the wisest decision. There’s just too much economic uncertainty out there, and, anyway, you’re always better off spreading your eggs across a few baskets. And, if you’re wondering which baskets, European and Japanese stocks could be worthy of your hard-earned money. Let’s take a look…

How have stocks in Europe and Japan done this year?

There’s been a ton of excitement about Japanese stocks and their gains this year. But, surprisingly, the pan-European index, the Stoxx 600, has outperformed Japan’s benchmark Topix index by nearly 2%. That is, if you’d invested (as many people do) in US dollars, without hedging the currency risk.

The total return of Japan’s Topix index (white line) and Europe’s Stoxx 600 (orange line) so far this year, in US dollars. Source: Bloomberg.

And this just shows how, year to year, currency fluctuations can have a huge impact on your returns. See, the Topix has returned nearly 26% this year in yen terms, and the Stoxx 600 has returned 15% in euros. But the yen has fallen roughly 11% against the US dollar this year, and that’s chipped away at the value of yen-denominated assets. The euro, meanwhile, has barely shifted at all.

The gains this year for Japan’s Topix, Europe’s Stoxx 600, the price of the US dollar versus the Japanese yen (USD/JPY), the euro versus the yen (EURJPY), and the euro versus the dollar (EURUSD). Source: Bloomberg.

Of course, you can avoid being knocked around by those currency swings by buying a “hedged” ETF when you invest. The WisdomTree Japan Hedged Equity Fund (ticker: DXJ; expense ratio: 0.48%) is one popular example.

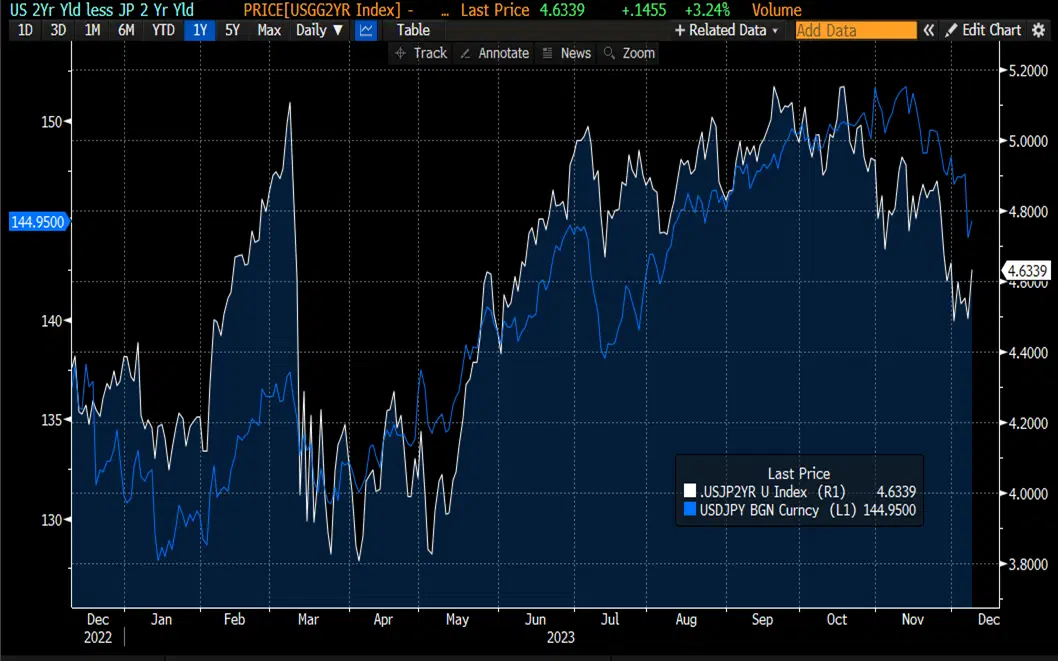

And you can understand why people would opt to hedge when it comes to the yen. See, most of the world’s economies have been jacking up interest rates to try to combat ultra-hot inflation, and Japan’s been doing the same thing – but to a far lesser extent. In fact, the Bank of Japan, whose major challenge in the past two decades has been deflation, has kept its overnight lending rate negative. So, 2-year Japanese bond yields have finally crept into positive territory, but they’re still at a paltry 0.09%, compared to the US 2-year, which is around 4.72% (and had been above 5% until just a few weeks ago). That difference has made the US dollar far more beloved among investors than the yen.

The difference in 2-year government bond yields in the US versus Japan (white line), and the price of a single US dollar, in yen (blue line). Source: Bloomberg.

What’s the outlook for Europe and Japan’s stocks, then?

Let’s take this in turns.

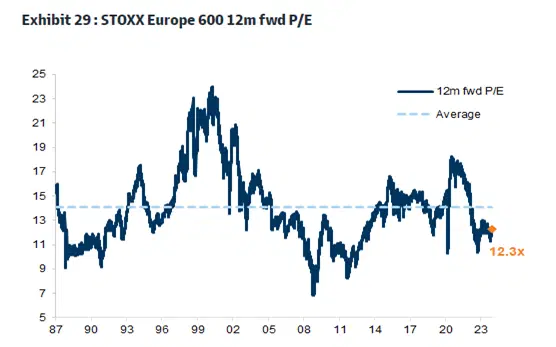

First, European stocks. The Stoxx 600 has rallied about 10% in the past six weeks, leaving it around 473, which is very close to where Goldman Sachs sees it ending next year. Its total return for 2023 – including dividends – has been a respectable 15% in both euros and US dollars, and even after this recent rally, Europe’s stocks remain cheap, relative to their history.

The Stoxx 600’s 12-month forward price-to-earnings ratio. Sources: Datastream, Stoxx, Goldman Sachs.

Without a doubt, Europe’s stocks have been hit hard by high inflation and sharp increases in interest rates. Russia’s invasion of Ukraine and the resulting high energy prices, plus the bloc’s trade reliance on a struggling Chinese economy, have all taken a toll on Europe’s stocks, dragging down their valuations.

But inflation has been falling in Europe, and Goldman sees it dropping to just 2.7% by mid-2024 – not terribly far from the central bank’s long-term 2% target. And that should have two positive impacts, Goldman says: for one thing, real wages (that’s pay after factoring in inflation) should be positive, which would boost consumer sentiment, and, for another, it should allow the European Central Bank (ECB) to cut rates, beginning in the second quarter of 2024.

Aside from those things, Goldman also says continued share buybacks in Europe and the fact that many investors have been broadly shunning these assets could help propel the Stoxx 600 higher. And if inflation manages to continue to fall without a nasty recession coming around, then Goldman says those European stock valuations will look even more tempting. And that’s when you might go for a mix of growth and value stocks. For that kind of balanced European stock exposure, the iShares MSCI Eurozone ETF (EZU; 0.52%) could be the right path.

Second, Japanese stocks. In yen terms, they’ve been amazing, rising on expectations that Japan has finally left its low-growth and multi-decade deflationary economy in the past. Corporate governance reform initiatives announced by the Tokyo Stock Exchange earlier this year have turbo-boosted the country’s stocks, with a steady flow of companies announcing measures to improve shareholder returns.

But, much of the stock performance this year has been driven by multiples expansions, not actual profit growth, so there is some room for disappointment here as valuations using price-to-earnings ratios are now a lot pricier.

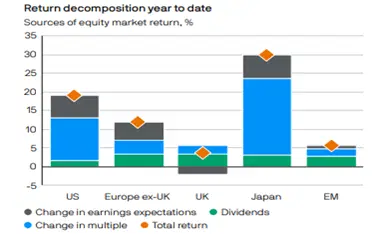

Here are the major sources of equity market returns this year, through November 15th. Sources: FTSE, IBES, LSEG Datastream, MSCI, S&P Global, JPMorgan Asset Management.

Goldman is forecasting earnings-per-share growth for Topix in the high single digits for both 2024 and 2025, and sees an end-of-year 2024 Topix target of 2,650, versus Tuesday’s close of 2,353. The investment bank says foreigners and corporations are likely to continue to buy more Japanese stocks than they sell, and the country’s retail investors are likely to follow suit, prompted by the government’s new investing tax incentives.

And there’s likely to be another big driver as well: the Bank of Japan is expected to remove its “yield curve control” in 2024, letting interest rates break out of their formerly restrictive narrow band and drift higher. At the same time, other central banks like the ECB, the US Federal Reserve, and the Bank of England are expected to cut interest rates.

Those two factors should shrink the difference between Japanese bond yields and those from other advanced economies, and boost the yen as it becomes more attractive for international savers and investors. But there are always a lot of moving parts in predicting currency moves, so if you do fancy investing in Japanese stocks, you might consider splitting your investment – some in a hedged ETF like the WisdomTree Japan Hedged Equity Fund, and some in an unhedged ETF like the iShares MSCI Japan ETF (EWJ; 0.5%).

-

Capital at risk. Our analyst insights are for information purposes only.

Russell Burns

Join the Investors' Club

Get access to professional investing tools for free and start building your wealth today!

Capital at risk