Think of TIPS as government bonds with a superpower: the bond’s principal (the original amount loaned), and its semi-annual interest payments, adjust with inflation rates.

If you hold them to maturity, you’ll be protected against inflation (your principal would rise with inflation) and deflation (your principal cannot fall below its original value), giving you certainty over what your capital will be worth in future dollars.

But, remember: TIPS are bonds, so their prices are exposed to interest rates (rising rates means falling prices), and that can sometimes offset the impact from inflation. But only if you don’t hold them maturity.

Treasury inflation-protected securities (TIPS) are one of the most overlooked and misunderstood assets out there. These clever US government bonds protect your investment against both inflation and deflation. And they could benefit handsomely from falling interest rates. That makes them a pretty interesting investment opportunity right now. So let’s take a closer look at TIPS and see why you might want to include them in your portfolio.

OK, what’s so exciting about TIPS?

TIPS are the US Treasury’s answer to beating inflation at its own game – think of them as government bonds with a superpower: the bond’s principal (the original amount loaned), along with its semi-annual interest payments, adjusts with inflation rates. And if you hold onto them until they mature, you’re looking at a money-back guarantee on your initial investment, no matter if inflation goes on a spree or takes a nosedive. That’s a double defense for your dollars, shielding you from inflation and deflation’s punches.

Picture this: You snag $10,000 worth of TIPS with a neat 2.5% annual interest. Now, let’s say inflation decides to jump up by 3% within a year. Here’s the play-by-play for your investment:

First, your TIPS will bulk up with inflation, boosting your principal by 3% to $10,300.

Next, your interest will get more

interesting

– it’ll be calculated at the beefier amount. So instead of pocketing $250 in yearly interest, you’ll be scooping up $257.50.

Finally, fast-forwarding to the year’s end (assuming that’s when the TIPS matures), you’ll walk away with your $10,300 principal and $257.50 interest, leaving you with a cool $10,557.50.

Now, let’s flip the script: imagine you invested that same $10,000 in TIPS, but now the economy hits a deflationary phase and the consumer price index (CPI) dips by 2%:

First, your principal will (temporarily) get a trim, shrinking to $9,800.

Interest will now do its magic on this slimmer figure, meaning your annual 2.5% interest payment will be just $245, doled out in two $122.50 helpings six months apart.

But here’s the TIPS kicker: these bonds come with a bottom-line promise that at maturity, you won’t get back anything less than what you put in. So if you’re playing the long game and you hold on until maturity, you’ll reclaim your full $10,000 original stake, plus the interest payments you’ve been pocketing, based on that interim deflated principal – a tidy $245 for the year.

And that’s what’s exciting about TIPS: the fact that holding them to maturity offers a unique shield for your buying power. If inflation climbs, so does your investment’s principal, preserving the real value of your money. And if inflation falls, your investment is protected too, as TIPS guarantee that you’ll receive no less than what you initially put in. This makes them a more secure bet than traditional bonds, which repay a fixed amount at maturity but can’t promise what that amount will be worth in future dollars. With TIPS, the principal may fluctuate, but the real value – what your money can actually buy – remains assured.

Certainly, TIPS come with their own set of complexities. If you sell them before they mature, the price you’ll get for them will depend on current market conditions, including prevailing interest rates and inflation expectations. These factors can significantly sway your returns – sometimes with surprising outcomes.

For starters, your principal is exposed to drops in inflation if you sell your bonds before they mature, as the guaranteed principal value applies only at the end date. Interest rates can have an even bigger impact: if they climb – perhaps because the Federal Reserve is tightening the reins to control inflation – the market value of TIPS can dip. That’s because, like all bonds, TIPS see their price fall as interest rates rise.

This can lead to a paradox where TIPS might lose value even when inflation is on an upswing. In fact, that’s precisely what TIPS holders witnessed over the past couple of years: inflation bumped up the principal, but rising rates pulled down prices, leading to overall losses. The bottom line is that while TIPS are a solid play for outlasting inflation in the marathon, they’re not the quick-fix hedge for a sprint. This doesn’t make them a bad investment: you just need to be clear on what your time horizon is.

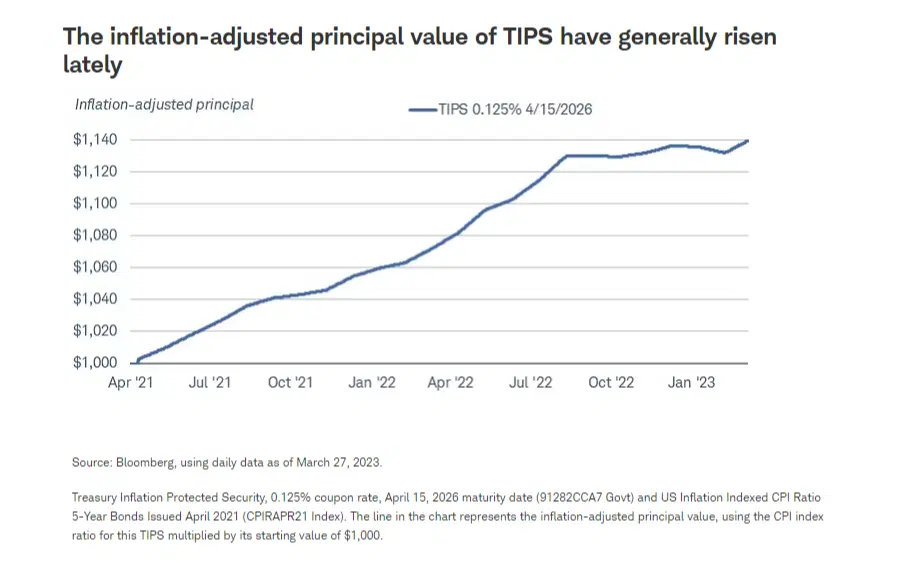

High inflation has bumped up the value of the principal of TIPS since 2021, but that increase has been more than offset as rising interest rates have pushed their prices lower.

Here are a few other factors to consider. Firstly, the TIPS market is quite small, so its pricing can swing with shifts in supply and demand – for example, when the US government opts to buy or sell a lot more TIPS. Secondly, these bonds are tied to CPI, a popular inflation gauge that might not reflect the full erosion of your buying power and, in some cases, could be subject to manipulation. Third, there’s usually a delay between realized inflation, and when it impacts the principal and the interest payments you’ll receive. Last, you have to pay taxes on the bond's inflation adjustments each year, even though you won't get that extra value until the bond matures.

What’s the opportunity here?

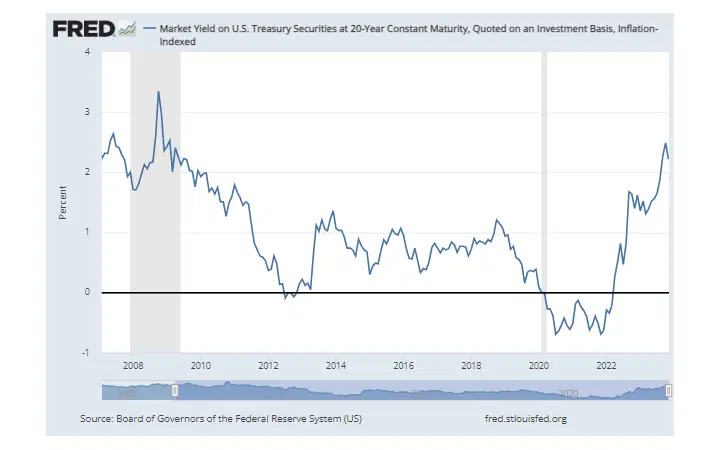

At present, with a real yield of 2.2% on a 20-year TIPS, you’re looking at a solid 2.2% real return (your nominal return will be 2.2% + the inflation rate) over two decades, with no inflation risk. Put differently, a buck invested in TIPS now is assured to maintain the buying power of $1.54 by 2043, no matter whether inflation soars or sinks, or whether the economy avoids a recession or tumbles right into the dreaded hard landing. Of course, the amount of money in interest payments you receive will shift in response to the ebb and flow of interest rates and inflation – as will the bond’s selling price should you choose to sell before it matures. But your principal is truly protected – in real terms – at maturity. And that’s pretty enticing in an uncertain environment.

What’s more, you’d have the option to sell your bond for a nice profit if the price rises before maturity. This could happen if investors start to expect sustained higher inflation, or if there’s a drop in interest rates. Unlike in 2021, when low yields offered a thin margin of safety, TIPS yields are sitting now at highs not seen in more than a decade. This makes a further rise in interest rates less likely, and provides a cushion in case inflation moderates toward more normal levels. And if interest rates drops, that’s when you could see the biggest profits – even if inflation dips slightly. And remember, if none of that happens, you could just hold your TIPS to maturity and pocket your initial investment at the attractive 2.2% real return.

Real yields are at attractive levels, providing investors with a cushion against falling inflation and with the opportunity to potentially profit from falling rates. Source: Federal Reserve Economic Data, or FRED.

Now, one might question the advantage of opting for TIPS over conventional “nominal” Treasury bonds. And, really, your decision should come down to where you expect inflation to go. To gauge the inflation rate that would equalize the benefit between holding a nominal bond and a TIPS, you can compare their yield differentials. That gap is called the “breakeven inflation rate” and represents what CPI would need to average over the life of the bond for TIPS to outperform Treasuries. Presently, with a yield gap of 2.3%, nominal bonds may appeal more to investors who predict inflation will trend below this threshold, while TIPS would be the choice for those expecting higher inflation rates. For investors who expect to see declining interest rates, a balanced approach may make sense: diversifying with Treasury bonds and TIPS. This blend allows you to hedge your bets, making your investment outcome less reliant on the unpredictable path of inflation.

OK, so how do you invest in TIPS?

One strategy is to purchase TIPS directly. They’re available from the US government via TreasuryDirect, an official website. It allows you to participate in auctions to buy newly issued TIPS for as little as $100. Or you can do it through a broker, which gives you the opportunity to secure both newly auctioned issues (“on-the-run”) and those circulating in the secondary market (“off-the-run”). Direct purchases grant you the flexibility to choose specific TIPS that align with your desired maturity dates, customizing your investment to fit your financial objectives. Plus, you’ll get semiannual interest payments that reflect the inflation adjustments made to your principal. And remember, if you hold them to maturity, those temporary price declines won’t matter, as you’ll always get at least the amount you initially put in.

Or, you can go the fund route and invest in a TIPS ETF. It’s a slick way to spread your risk across a pool of inflation-protected bonds and maturities, and keep things flexible – you can trade shares on the go, stock-style. But these ETFs can be a bit of a mixed bag: your payouts come as dividends, which can be a jumble of interest, gains, and even manager discretion, so not the steady interest stream you’d get from straight-up TIPS. And you’ll want to watch out for those management fees too, they’ll take a nibble out of your earnings. And remember, ETFs are forever rolling with the market’s punches, there’s no set cash-out date. So if interest rates do the tango, your ETF’s value will dance along with them – unlike a solo TIPS bond, which just does the wallflower thing until maturity. The iShares TIPS Bond ETF (ticker: TIP; expense ratio: 0.19%) is a diversified choice. For a longer maturity, you could consider the PIMCO 15+ Year US TIPS Index ETF (LTPZ; 0.20%).

Join the Investors' Club

Get access to professional investing tools for free and start building your wealth today!

Capital at risk